Is 8% Growth Good? The 2025 Agency Benchmark Is 10.7%

Craig and Jason are licensed P&C agency owners, co-authors of Million-Dollar Agency, creators of the trademarked Telefunnel, hosts of The Insurance Dudes podcast, and speakers.

Written and reviewed under our editorial process. Found an error? See our corrections policy.

Best Practices independent agencies hit 10.7% organic growth and 26.1% EBITDA margins in 2025. Here is what those numbers mean for your agency, why the gap is operational rather than luck, and which specific benchmarks to measure against right now.

TL;DR

Best-Practices independent agencies posted 10.7% organic growth and 26.1% EBITDA margins in 2025, and the gap to the average agency is operational, not luck. The Big "I" and Reagan Consulting study ties that gap to measurable thresholds: organic growth rate as the real health metric, the Rule of 20 (a record 25.1 in 2025), producer-development investment held near 2% of revenue, and revenue per employee. Read your own numbers against these benchmarks to find where growth is leaking and which lever to pull first.

Independent agencies at Best Practices level hit 10.7% organic growth and 26.1% EBITDA in 2025. The gap between those firms and the average is not luck: it is measurable, tied to specific operational thresholds in sales velocity, producer investment, and revenue per employee. Every number in the Big "I" and Reagan Consulting 2025 Best Practices Study has a practical meaning for your business. Here is how to read them.

Why does your agency's organic growth rate matter more than total revenue?

Revenue tells you how big you are. Organic growth tells you how healthy you are. An agency growing at 4% through rate increases alone is losing ground. The Best Practices framework, which has tracked the top tier of independent agencies for 32 years in a joint study between the Big "I" and Reagan Consulting, focuses on organic growth as the primary health indicator because it strips out acquisitions and pure rate inflation and measures what you actually built.

The broader market gave every P&C agency a tailwind in 2024. According to the Big "I" 2025 Market Share Report, direct written premiums across the P&C market reached $1.05 trillion in 2024, up from $952 billion in 2023, a 9.6% increase that pushed combined ratios down to 92% from 96% the prior year. The NAIC's 2024 property and casualty market data confirms the scale: with roughly 84% of companies reporting, the industry had already logged nearly $975 billion in direct written premium.

Independent agencies captured the core of that market. The Big "I" Market Share Report shows the independent channel placed 61.5% of all P&C insurance written in the U.S. in 2024, including 87.2% of commercial lines and 39% of personal lines. But placing volume is not the same as growing profitably. The question is how much of that market growth your agency actually converted into durable organic revenue.

What organic growth percentage separates a Best Practices agency from an average one?

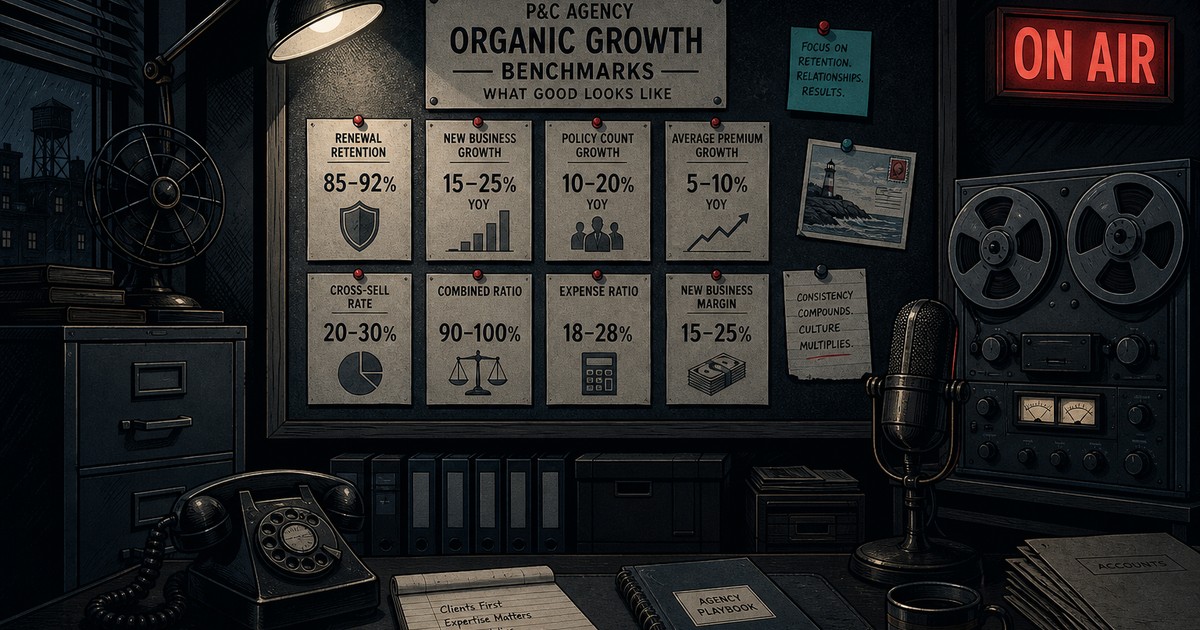

Best Practices agencies posted 10.7% organic growth in 2025, according to the Big "I" and Reagan Consulting study. That figure includes strong personal lines and group benefits performance, with commercial P&C moderating in most revenue categories as rate increases slowed.

The study itself notes that "the industry has never been healthier" at the top tier. But Best Practices firms are not average firms. They are nominated, vetted agencies that represent a ceiling of performance, not a median. The gap between a Best Practices firm at 10.7% and an average agency running 4% to 6% organic growth is the difference between compounding your business value and treading water.

IA Magazine's coverage of the same study emphasizes that the results span agencies from under $1.25 million to over $100 million in revenue. Scale is not the differentiator. The agencies that qualify at every revenue size share the same operational disciplines, not the same client count.

What is the Rule of 20 and why did it hit a record 25.1 in 2025?

The Rule of 20 is the most useful single number the Best Practices study produces. It is calculated by adding your organic growth rate to 50% of your pro forma EBITDA margin. A score above 20 signals a healthy agency; scores above 25 are exceptional and correlate directly with strong acquisition valuations and perpetuation options.

Best Practices agencies hit a Rule of 20 score of 25.1 in 2025, according to the Reagan Consulting and Big "I" study. To generate that number, you need both sides of the equation. The 2025 cohort delivered 10.7% organic growth plus EBITDA margins of 26.1%. Drop either lever and the score deteriorates fast. An agency at 5% organic growth would need EBITDA over 40% to reach 25, which is not realistic without severe underinvestment in people and production.

EBITDA at 26.1% also tells you that top agencies are not sacrificing profitability to buy growth. They are doing both simultaneously, which means their cost structure and sales systems are efficient enough to grow the top line without proportionally expanding overhead.

How much should an independent agency invest in producer development each year?

The Best Practices study tracks NUPP: net unvalidated producer payroll, a measure of how much an agency is investing in producers who have not yet validated their production, expressed as a percentage of total revenue. According to the 2025 study, NUPP held at 2.0% in 2025, up from 1.9% in 2024. The study identifies 1.5% to 2.0% as the healthy target range.

What does that mean in practice? An agency doing $3 million in revenue should expect to carry $45,000 to $60,000 in payroll for producers who are not yet paying for themselves. That is a real cost. Agencies that shrink NUPP below 1.5% are essentially cutting off their future growth pipeline. Agencies that let it drift above 2.5% without a structured ramp program are burning cash on producers who are not progressing.

Producer recruiting is the structural constraint here. The Q1 2025 Insurance Labor Market Study by the Jacobson Group and Aon's Performance Benchmarking Division, as reported by Program Business, found that 55% of insurance companies planned to expand their workforce over the following 12 months, with technology, underwriting, and claims roles in highest demand. For independent agencies competing against carriers and larger brokers for the same candidate pool, this means recruiting must be a continuous investment, not an emergency response.

The P&C workforce outlook heading into 2026 shows demand continuing to increase. PropertyCasualty360's 2026 workforce forecast notes that insurance job openings are expanding, putting more pressure on agencies that wait until a seat opens to begin their candidate pipeline.

What does revenue per employee tell you about your agency's operational health?

Best Practices agencies averaged $228,321 in revenue per employee in 2025, per the Reagan Consulting study. That number went up from prior years despite the fact that average compensation per employee also increased. Revenue grew faster than headcount and payroll, which is the only sustainable path.

If your agency is below $180,000 per employee, you have a capacity and systems problem. The work is not generating enough revenue per seat to fund both compensation and investment. Common causes: producers carrying too many service tasks, CSRs processing work that could be automated, or account structure that mixes high-touch commercial accounts with low-margin personal lines without the right staffing ratio to support each.

Sales velocity is the other side of this. The study identifies a 12% to 13% sales velocity threshold as the minimum for a healthy sales culture, and Best Practices agencies exceeded that threshold in all revenue categories in 2025. Sales velocity measures new business production as a share of existing revenue. Below 12%, you are not replacing lost accounts fast enough to grow; above 15%, you are compounding.

How do producers and hiring decisions directly affect organic growth outcomes?

You cannot build an agency that grows at 10%+ without a functioning production machine. The NUPP investment and the sales velocity benchmark only work if the people you are investing in are the right people, placed in a structure that lets them sell.

Agencies that struggle with recruiting share a common pattern: they treat it as a one-size-fits-all activity and let urgency override their quality filters. The result is that NUPP investment flows to the wrong hires and produces nothing. The Big "I" hiring and recruitment resources were built specifically to give independent agency owners structured tools for recruiting and assessing producer candidates before urgency distorts the process.

For a more detailed look at building a producer pipeline before the seat opens, see this earlier post on the producer pipeline framework. For the agency-wide growth system that connects hiring, sales process, and operations into a single framework, see the 5 P's of P&C agency growth.

Two actionable takeaways from the 2025 Best Practices data:

First, if your Rule of 20 score is below 20, identify which side of the equation is dragging it down. If organic growth is under 8%, the problem is in sales velocity and producer investment. If EBITDA is below 18%, the problem is in cost structure and revenue per employee.

Second, treat NUPP as a deliberate budget line, not a residual. Decide what percentage of revenue you are committing to unvalidated producer payroll before you need to fill a seat, and recruit continuously so that a resignation does not force a reactive hire that bypasses your quality filters.

What is the bottom line on using the 2025 Best Practices benchmarks to close your agency's growth gap?

The Big "I" and Reagan Consulting 2025 Best Practices Study is not aspirational reading. It is a calibration tool. Every number in it: organic growth at 10.7%, Rule of 20 at 25.1, EBITDA at 26.1%, NUPP at 2.0%, revenue per employee at $228,321, and sales velocity above 13%, is a specific target you can measure against your own P&L today.

The independent channel placed $1.05 trillion in P&C premium in 2024 and captured 61.5% of the total market, according to the Big "I" Market Share Report. The opportunity is there. The agencies converting market opportunity into durable growth are doing it by managing to benchmarks, not by hoping the market keeps inflating.

Pick one number. Measure it. Fix the system underneath it. Repeat.

Sources cited in this analysis?

- Big "I" and Reagan Consulting 2025 Best Practices Study - organic growth, EBITDA, Rule of 20, NUPP, revenue per employee, sales velocity

- Big "I" 2025 Market Share Report - 61.5% IA channel share, $1.05 trillion DWP, commercial and personal lines splits

- NAIC 2024 Property/Casualty Market Share Data - P&C market scale, reporting data

- Program Business: Insurance Workforce Trends in 2025 - Q1 2025 Labor Market Study by Jacobson Group and Aon, workforce expansion and hiring outlook

- IA Magazine: Big "I" and Reagan Consulting Release 2025 Best Practices Study - Best Practices study coverage

- PropertyCasualty360: 2026 Trend Forecast - The insurance workforce - workforce openings outlook

- Big "I" Agency Hiring and Recruitment Resources - structured tools for independent agency producer recruiting

Listen to The Insurance Dudes Podcast

Get more strategies like this on our podcast. Available on all platforms.

Related Episodes

Brett Young's Mega Agency Playbook for Scale (Part 2)

Matt Dietz: From Survival to Scale in His Agency (Part 2)

Operators Die, Owners Leverage: Working On vs In Your Agency

Brett Young on What It Takes to Build a Mega Agency (Part 1)

Laura Harris Built an Agency That Runs Without Her